In-depth articles, series and guides

In-depth articles, series and guides

In 2023, I decided to quit my full-time job and focus completely on a side business I had been running for a few years.

This decision, however, came with a financial challenge. It meant my wife and I had to reduce our household spending to a sensible level so we wouldn't run out of cash before the business started flying.

Three years later, I'm still amazed at just how much we've been able to cut our monthly expenses without significantly downgrading our lifestyle.

In this blog post, I'll share everything we did and still do to keep our spending under our ideal target budget, and how you can tweak the core ideas to work for you.

Let's start by:

Getting a lay of the land

Before we could trim the fat, we needed data to point us in the right direction. This is where our long-standing habit of tracking daily expenses came in handy.

For years, my wife and I've been diligently tracking our spending through a quick and simple system:

Whenever we spend money on anything, whether that's buying something or paying for rent, utilities, food, etc., we note it down.

A spreadsheet does an okay job for this, but we use the Ducat app to make things easy to note and visualise later.

So, upon making a purchase, we describe the expense in the app, and it gets logged with an appropriate category from our list, along with a relevant note:

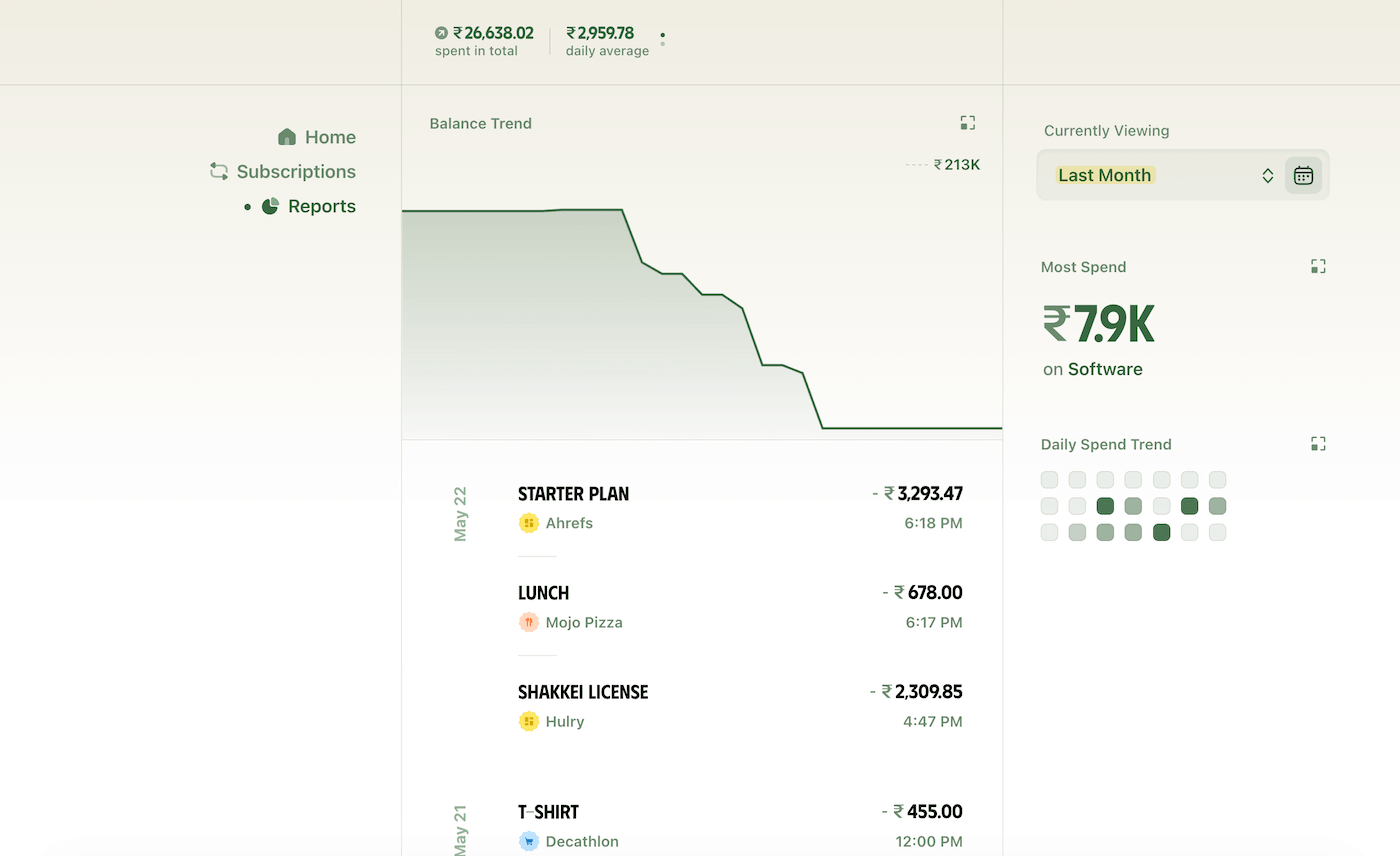

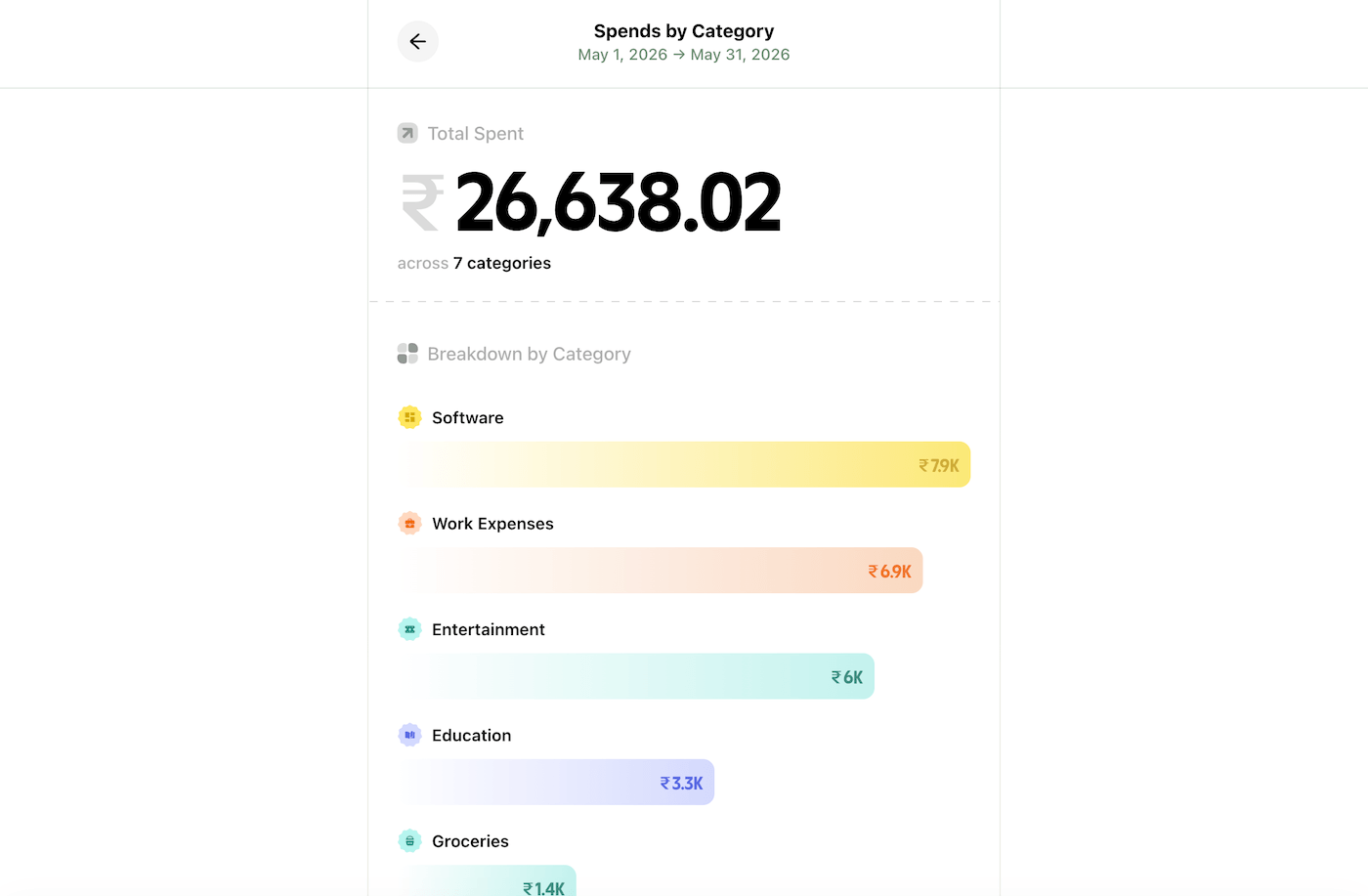

Later, when we're ready to reflect on our financial habits and decisions, we review our expenses scoped within a time period, such as last month:

And also, see our spending during that time, grouped under categories:

This is what we did in 2023.

Since we've been tracking our expenses for years, we combed through our spending data to spot all the ways we've been excessively spending our monthly income.

The Ducat app didn't exist 3 years ago, so we used a different app then.

One area that immediately jumped out was that we were spending too much money every month on restaurant food.

We did cook at home, but we were ordering food too liberally at the slightest hint of laziness, and that was costing us a good portion of our monthly income.

The next area was online shopping.

Although we have been quite restrained in blowing money on moderately useful stuff for a long time, we occasionally made impulse purchases.

Reducing the frequency of those impulse purchases would not only help us save money, but we could also use a portion of that money to buy goods that we would actually use and derive value from.

Now, by this point, we had identified our one-off purchases.

But nowadays we all have a few subscriptions that bleed us money every month or year, even if we aren't using the service or product much.

For example, I had a monthly subscription to the Adobe Photography Plan, which included access to Lightroom and Photoshop.

I used the apps probably 4–5 times a year, especially after returning from a trip, but I was paying a monthly fee to maintain them for those “when I need them” moments.

The monthly fee wasn't huge, but when you tally up the yearly cost, especially over many years, they add up. And if you aren't getting much value from the service, then it's simply money down the drain, on autopilot.

This is where an app like Ducat comes in handy.

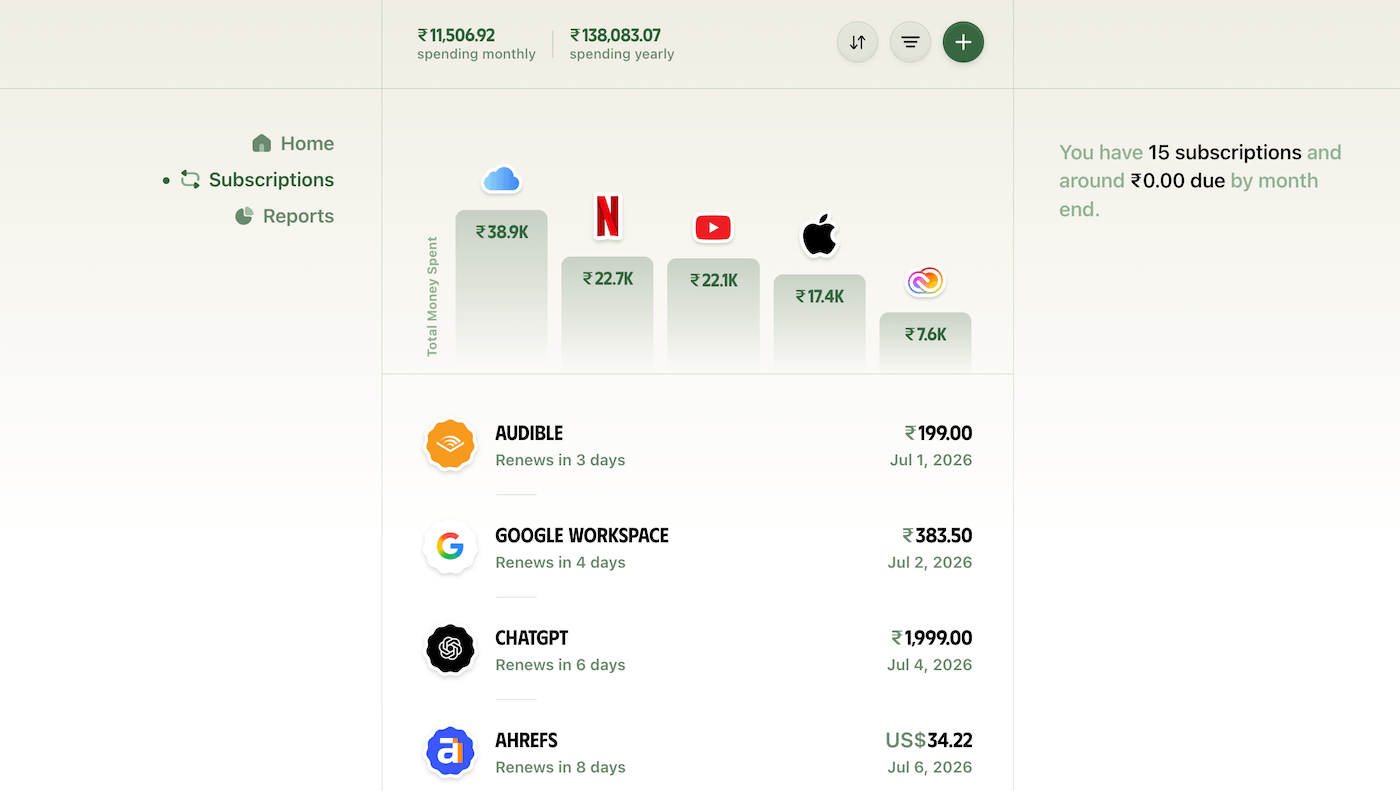

We've been tracking our subscriptions in the Ducat app for a while, and it now gives us a clear picture of every active subscription we hold, how much we're spending every month, and how much we've cumulatively spent on our top subscriptions to date:

I never realised I had spent over ₹22,000 (~$233) each on Netflix and YouTube Premium over the years. The snowballed impact of a small monthly fee wasn't visible all these years.

I wish I had had this view three years ago, when we manually projected our subscription costs, but well, this will be helpful in our ongoing efforts to keep our spending in check.

Now, with a solid understanding of where our money was going every month, we decided on these:

Three key measures

First, more cooking at home, and less ordering in.

We reduced our frequency of eating out or ordering takeaway, which cut our spending to 1/4th of what it was before.

We also made a modest investment in getting an air fryer. The air fryer allows us to cook many of the dishes we were ordering in before, and we now enjoy much better versions of those dishes at home while spending far less money.

Second, we leaned heavily on the concept of conscious spending.

I discussed the concept of conscious spending in a previous article and a video about the three questions I ask myself before buying anything:

This framework has played a significant role in how we allocate money to buy things that serve us well instead of blowing money on every shiny new thing we come across.

Third, we realised our lightly used subscriptions had to go.

Now, while trying to cancel the Lightroom subscription I mentioned earlier, Adobe introduced me to a lower-tier subscription that was a solid middle ground.

I would be paying less than half the previous billing amount, but keep access only to Adobe Lightroom, which is the only app I use anyway.

Therefore, instead of cancelling the subscription altogether, since I use it occasionally, I moved to a lower tier and saved significant money without downgrading my experience.

If a service doesn't offer a more suitable lower-tier on cancellation, ask their support or do some exploration.

With these tiny but consequential changes, we had reduced our spending by nearly 40%, which was a huge help in sticking with my initial decision of moving to my business full-time.

Now, while these one-off measures work well, a long-term solution requires:

A periodic retrospection

We knew that if we didn't make a habit of regularly reviewing our expenses, we would soon fall back into our old spending habits.

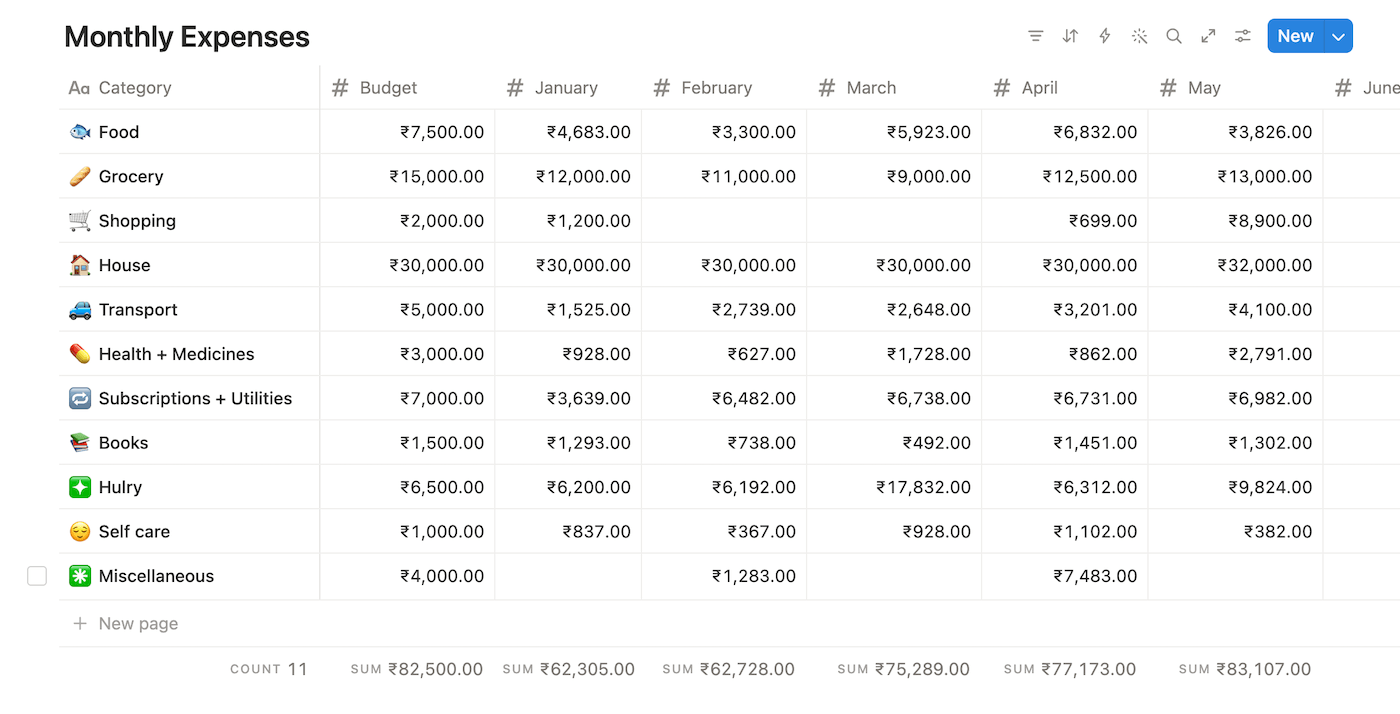

Therefore, my wife and I created a yearly view of our spending on a shared Notion page where we started noting our monthly spending, grouped by relevant categories:

We use the Ducat app to first gather the data, as everything is tallied by groups already.

Then, copy those figures into the Notion database.

Since every category doesn't make sense to note here, we put occasional spends under a Miscellaneous category in the Notion database.

The beauty of this table is that it helps us see a side-by-side comparison of our monthly spending across a year.

We can identify which months went beyond our ideal spending quota, and what the root cause was.

Therefore, if we identify that we have spent too much on, say, shopping this month, we'll try to rectify that the next month unless there's a necessary purchase in the pipeline.

My wife fills in the column for the previous month on the first day of a new month, and we then take 5–10 minutes to review our spending.

It's a lightweight process that yields dividends in keeping our household expenses in control.

Now that we've discussed the process, here's:

An action plan for you

The first step to any cost-cutting plan is to know exactly where you're spending too much and what you want your ideal spending amount to be.

Goals like “I'll spend less from next week” don't work because they're vague, don't give us a clear path forward and therefore, are easy to discard.

So, before you begin strategising, collect your spending data.

This becomes easy if you have already been tracking your expenses somewhere. You can pull in that data.

But even if you're new to this, there are a few options:

- You can spend a month diligently tracking your daily expenses in a spreadsheet or an app like Ducat. Track everything regardless of the amount. Then, once you have enough data after a month, use that data to identify where you're usually leaking money.

- If you want to get started right away, you can look at your bank statement, and depending on how far back you can remember, sort the transactions with notes and categories to form your initial data set.

While you're gathering this data, don't forget your subscriptions, if you have any. These are often the largest source of wasted money because we subscribe for a small monthly fee and then forget to cancel, or don't even notice the monthly spend amidst other daily expenses.

With the data in hand, see where you can meaningfully reduce your spending without downgrading your lifestyle too much.

Now, how much you cut depends on how cash-strapped you are at the moment and what your ideal future budget amount looks like.

For example, when we were cutting our spending, we calculated an ideal maximum monthly budget that we would not like to overshoot any given month. Since life's random and unexpected expenses happen, we added around 20–30% buffer budget to the monthly amount, and that became our target.

You can follow something similar, or use your own calculation.

Finally, once you have successfully cut your spending down to your ideal budget, keep a monthly review going.

Where the monthly review helps is that it continuously allows you to course correct at a monthly level, without becoming a frequent overhead.

Try these out, and I'd like to close this piece with a thought:

I've often seen people recommending increasing income over cutting expenses as a better financial approach.

While that works for some people, I believe, even if you increase your income, it's prudent to keep your expenses in check, because lifestyle creep can shoot up fast as you make more money, and you end up in the same position all over again.

With diligent tracking and conscious spending, we can ensure we're putting our money to serve our best interests.

Good luck.